R&D LOSS TAX CREDIT

RESEARCH AND DEVELOPMENT LOSS TAX CREDIT

Tax relief is available for loss-making, R&D intensive start-up companies. Eligible companies are able to "cash out" tax losses from R&D spending. The tax relief takes effect from the 2015/16 income year (1 April 2015). The intention of the scheme is to provide New Zealand based, R&D intensive start-up companies with an early "cash out" option for their R&D tax losses. Eligible companies will have "early access to all or part of their tax losses in the form of a cash receipt, rather than carrying those losses forward”. These companies are able to cash out the lesser of:

- 1.5 times the company’s R&D expenditure on salaries and wages;

- Total losses;

- Total qualifying R&D expenditure; and

- The cap on eligible losses each year will initially be 28% of $500,000 of losses; rising over time to 28% of $2 million of losses.

Statement of R&D Activity and Expenditure

The IRD require that a statement of R&D activity and expenditure is prepared by claimants. The IRD advise the purpose of the statement is to establish eligibility by detailing the nature of R&D activity and the amount of qualifying expenditure. Companies will be required to provide information in the statement that confirms they are eligible for a "cash out". The information required includes:

- Details of the R&D activity that shows it meets the accounting definition of R&D;

- Evidence that the R&D is being undertaken in New Zealand;

- Salary and wage expenditure that relates to R&D; and

- Details of the company grouping, shareholding or ownership.

Claims will be screened to discourage fraudulent claims. Enough detail will need to be provided to allow checks to take place. The comprehensiveness of the screening process will need to be balanced against greater administration and compliance costs for companies.

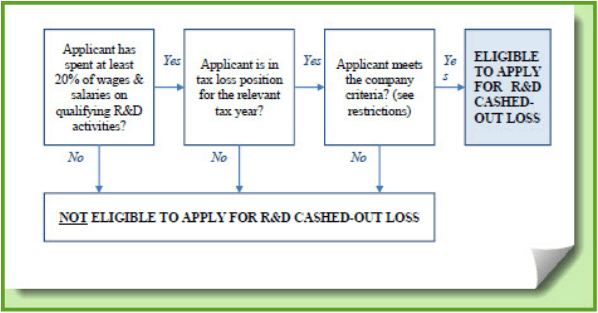

In most instances, it will be possible to make a payment based on the information provided in the statement of R&D, along with other information already held by Inland Revenue (such as PAYE schedules). This will minimise the additional compliance burden placed on taxpayers. In some cases however, further screening and investigation may be needed. The diagram below, prepared by the IRD, summarises the various criteria determining whether an applicant would be eligible for the cash-out proposal.

In most instances, it will be possible to make a payment based on the information provided in the statement of R&D, along with other information already held by Inland Revenue (such as PAYE schedules). This will minimise the additional compliance burden placed on taxpayers. In some cases however, further screening and investigation may be needed. The diagram below, prepared by the IRD, summarises the various criteria determining whether an applicant would be eligible for the cash-out proposal.

Eligibility Flow Chart

Calculating R&D Expenditure

The IRD provide guidelines on how research and development expenditure is defined and what costs are eligible for the tax credit. They refer to accounting definitions of R&D including FRS 13 and NZIAS 38. Eligible R&D expenditure is specified for a reporting period and includes salaries and wages of employees wholly or partially engaged in R&D, overheads apportioned to R&D, materials and consumables used in R&D, depreciation and external expenditure on R&D experts, consultants and contractors. The IRD also publish specific exclusions. For example providing a service of R&D to another person or work involved in reproducing existing product or process, for example reverse engineering. We can provide claimants with a framework and a template on how to calculate R&D expenditure and how to prepare, maintain and substantiate R&D records.

Registering Interest

To start with you can register your interest in applying to cash out your company's R&D losses with the IRD. They IRD will confirm if your company meets eligibility requirements.